Investor Sentiment, Market Timing and Futures Returns by Changyun Wang

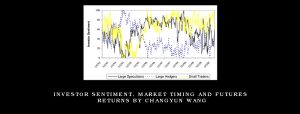

This study examines whether the sentiment index based on the operator’s real position is useful for predicting the futures market returns of the S&P 500 index. The results show that the great speculative sentiment is an indicator of price continuation, while the Great coverage sentiment is a contrary indicator. Small-trader sentiment hardly predicts future market movements.

Furthermore, the sentiments of the great extreme traders and the combination of the sentiments of the great extreme traders tend to provide more reliable forecasts. These findings suggest that large speculators have superior synchronization capabilities on the market.

Also Get Investor Sentiment, Market Timing and Futures Returns by Changyun Wang on Traderknow.com

Visit more course: BOND – STOCK TRADING

The same course: Djellala – Training by Ebooks (PDF Files), Also StratagemTrade – Rolling Thunder: The Ultimate Hedging Technique. Also Tom K. eloyd – Successful Stock Signals for Traders and Portfolio Managers: Integrating. Daniel T.Ferrera Llewelyn James Martin Armstrong investorsunderground

Available at traderknow.com

Please contact email: [email protected] If you have any question.

Course Features

- Lectures 0

- Quizzes 0

- Duration 50 hours

- Skill level All levels

- Language English

- Students 182

- Assessments Yes